Welcome to the second edition of Field Notes, a quarterly newsletter from EdenTree’s Sustainable Investment team. Curated and led by a different member of the team each quarter, this newsletter provides a snapshot of our current key areas of focus: the stories holding our attention, the developments impacting our sector and the conversations shaping our work.

As EdenTree’s lead on proxy voting and corporate governance, I’m delighted to kick off our second edition with some half-time reflections on proxy season. Overall, the 2026 season has reminded us that while the items on the ballot are important, the terms on which investors are allowed to participate are even more so.

In this edition:

- Proxy season reflections

- PFAS and hazardous chemicals engagement

- SEC reporting changes

- Bank climate accounting trends

- AI workforce transition

We hope you enjoy the read. Again, we’d love to hear from you with any feedback, questions, or topics you’d be interested in seeing explored in future editions, so please get in touch.

- Hayley Grafton

Half-time analysis: pressure building in the proxy arena

Each year, proxy season stands out as a real source of insight for the team, and 2026 hasn’t disappointed us yet. In our view, the clearest theme to come out of the season so far has been the continuing shift in the power balance between shareholders and companies. While this has been building for a few years now, a more permissive regulatory backdrop in the US has accelerated the trend. In the UK and Europe, tensions are less pronounced, but present nonetheless.

Against this backdrop, the core questions for EdenTree remain the same: are boards delivering on credible strategies, are directors being properly held to account for lapses in oversight, and are shareholder rights being protected, or are they seen merely as an inconvenience to be engineered around?

Credible strategies: The most interesting votes are often the ones that test the resilience and suitability of a company’s strategy in practice. At Alphabet, the rapid build-out of AI infrastructure has brought data centres into the spotlight. Shareholders are asking how much power and water this growth will require, where it will come from and just how that sits alongside existing climate commitments.

Director accountability: BP has offered one of the clearest examples of the role judgement plays in governance. The removal of the company’s chair so soon after appointment has raised questions about succession and board culture, both issues in which investors need confidence that directors are willing and able to act when oversight comes under strain or fails.

Shareholder rights: Though unrelated to the proxy season itself, the upcoming wave of AI IPOs will likely have an impact on company structures and shareholder rights in future seasons. The much-hyped IPO of Space X has created a governance framework that concentrates power firmly in the hands of Elon Musk in support of his broader interests while reducing the protections available to minority investors. We are also concerned by Nasdaq’s recent rule changes, which, if applied to a company like Space X, could create unwanted impacts for passive investors including savers and pension beneficiaries.

Taken together, these examples serve to illustrate why proxy season remains such a useful window into the market. The votes matter, but so too do the structures, disclosures, board decisions, and wider context around them.

Engagement & Voting: In Brief

From issuer alignment in sustainable debt to PFAS phase-out, our stewardship work this quarter centred on emerging areas of risk and accountability.

- Attending the Environmental Finance Sustainable Debt EMEA Conference provided a valuable opportunity to hear from fellow sustainable debt investors and directly engage with several companies in a less formal setting to our structured engagement approach. We met with German development bank KfW to learn more about project due diligence to minimise human rights risks, French rail group SNCF to learn more about social inclusion and additionality, and UK social housing organisation Peabody to better understand how it considers impact as part of its development pipeline, as well as how it manages issues related to tenant vulnerability and wellbeing.

More broadly, the conference underscored the broader developments we have been observing as investors. While labelled bond issuance continues to be dominated by green bonds (c.60%), the mix of labels is evolving, with subcategories such as blue and transition bonds gaining traction. Regulation, particularly in Europe, was generally seen as a net positive, providing important guardrails, although its application remains unevenly applied globally. There were also signs of a consensus around the importance of issuer-wide alignment with intended impacts (beyond the bonds themselves) and greater scrutiny of impact measurement beyond reach-based metrics. - We have been engaging with our chemical company holdings on hazardous chemicals and PFAS phase-out, as the negative human and environmental impacts of chemicals that do not break down are increasingly material. As part of our work with the Investor Initiative on Hazardous Chemicals, we recently spoke with Yara to encourage greater transparency on hazardous substance exposure and the feasibility of substitution or phase-out. Yara is reviewing its exposures and monitoring where phase-out may be feasible; we encouraged the company to strengthen disclosure and publish its internal PFAS statement, including confirmation that it does not produce persistent chemicals.

The materiality of PFAS phase out can be demonstrated by recent litigation in Australia, where the government has launched a $2bn claim against 3M over PFAS contamination from firefighting foam, highlighting the growing legal and reputational risks associated with hazardous chemical exposure. Later this year we will continue our engagement across the chemical sector, pushing for stronger water stewardship as scarcity and pollution risks become increasingly material to both affected communities and the long-term resilience of the sector.

For more examples of our recent stewardship activity head to our quarterly Sustainable Investment Activity and Proxy Vote Reports.

On Our Radar

Topical news and research that has caught the team’s eye:

The future of quarterly reporting

The SEC has proposed a significant change to US market disclosure rules, allowing public companies to opt out of mandatory quarterly reporting. The stated aim is to reduce reporting burdens and support long-term decision making, however the proposal raises concerns around transparency and market fairness. The key question is whether less frequent reporting would genuinely support long-term decision-making, or would instead weaken accountability and widen information asymmetries between companies, insiders, institutional investors, and retail investors.

As outlined in a recent letter to the SEC by online community r/wallstreetbets1, retail investors rely far more on public filings due to lacking the access to management meetings and alternative data held by institutional investors. The risk is that reducing mandatory reporting ultimately redistributes timely information towards those already better equipped to access it.

Pace of global development slows2

In May, the World Bank published its Atlas of Global Development for 2026. The report, which tracks progress over the past 75 years, presents a troubling picture of both slowing developmental progress and deep and persistent inequality between high- and low-income countries.

- Global progress: Progress is now the slowest since records began for 15 of 26 key development indicators, with South Asia an exception globally

- Prosperity: Roughly 4 in 5 people live on less than $28 a day, considered the global prosperity standard

- Planet: Roughly 50% of the world’s population face water challenges

- Infrastructure: 1 in 2 live without electricity

- Digital: 1 in 4 does not use the internet

Regionally, perhaps the most troubling downturn has been in North America, where average progress across six core indicators has fallen sharply since the credit crisis and the aggregate development index for the region has been in reverse since before Covid. At a global-social level, particularly troubling has been the sharp fall in the “women political empowerment” index. Positive conclusions are hard to draw, and the report raises serious questions about structural inequalities and the systemic shortcomings that should be at the forefront of capital allocators’ minds. The need for a systems-thinking approach to investing and stewardship has never been greater.

Climate risks in financial accounting3

Despite worsening physical climate risks, banks continue to inadequately reflect climate risks in their financial accounts. While many increasingly acknowledge climate risks more generally, this tends to be long-term and is not yet translating into core financial metrics, with post-model adjustments typically minimal or absent. This has created a disconnect between the risks investors observe and those reflected in accounts, limiting incentives for banks to adjust lending or more carefully consider risk exposure. In a letter recently written to major banks and regulators (including the FRC and ICAEW), investors called for a review into the way banks reflect material climate risks and for improved disclosure of methodologies, assumptions and scenario analyses across the bank’s reporting.

The Need for a Responsible AI Workforce Transition

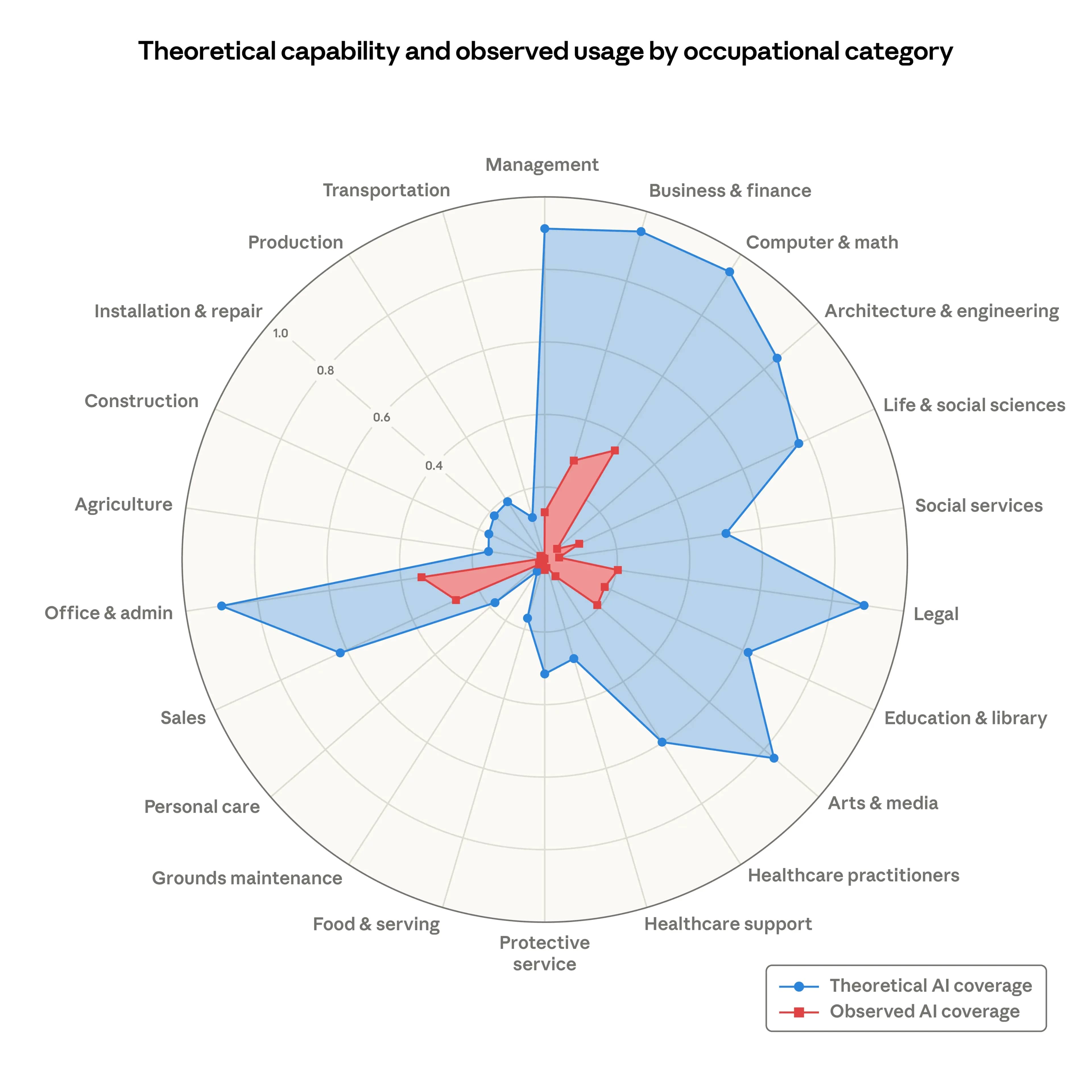

In a period dominated by headlines of trillion-dollar AI giants and the transformational power a handful of companies are having on the modern world, it is worth reflecting on what this means for the broader workforce and what a responsible workforce transition should look like if AI materially reshapes, or reduces, certain roles. As the image below highlights, these impacts will not be evenly distributed, with studies predicting some white-collar, administrative, financial, technology and professional-service roles are more likely to be reshaped by AI.

The concept of a “just transition” was developed to ensure that social interventions sit at the heart of decarbonisation, so that communities are not left behind by the move from fossil fuels to renewables. That same principle should surely be applied to the workforce most exposed to significant transformation from AI technologies.

While the UK government is encouraging AI upskilling, and redundancy protections already require employers to consider alternatives before dismissal, there remains limited emphasis on whether how companies, and their boards, are managing AI-related workforce change.

We increasingly see a role for investors in setting expectations for a “just AI” workforce transition, especially in highly affected sectors. Poorly handled AI-led restructuring can create operational disruption, reputational risk, loss of institutional knowledge and weaker employee trust. Expectations should therefore include board oversight of AI impacts, early workforce risk assessment, worker consultation, retraining and redeployment pathways, support for affected employees and post-exit outcome monitoring. This is not a new idea – SSE has shown what good looks like in its transition to renewables – but it now needs to be applied more widely to AI-exposed sectors.

Source: Theoretical capability and observed exposure by occupational category

Sources:

- Comments of /r/wallstreetbets

- Tracking Progress in Global Development | Atlas of Global Development

- HSBC convenes meeting of UK banks over climate risk

About Us

EdenTree is an active investment management house dedicated to sustainable and impact investing – it’s all we do. We have a 35+ year track record in this space, having launched our first ethical fund in 1988.

Our Sustainable Investment Team, made up of our fund managers and sustainability analysts, is united by four core beliefs that guide everything we do. We invest for a better tomorrow, acting as long-term, active investors who focus on businesses making a positive contribution to people and the planet. We invest in quality, combining rigorous investment and sustainability analysis to tilt our focus towards resilient and responsible companies. We invest at sustainable valuations, always considering the long-term value an investment can deliver for our clients. And we engage for change, maintaining an active programme of engagement and voting to ensure businesses are operating responsibly.

As of February 2026, every EdenTree fund carries an FCA Sustainability Disclosure Requirements (SDR) Sustainability label, reflecting the consistency and rigour that underpins our approach to sustainable investment. Our commitment to excellence in sustainable investing is further portrayed by our award wins, reflecting our leadership in sustainable finance and our inclusive culture. In 2025, we were awarded Best Ethical Investment Provider at the Investment Life & Pensions Moneyfacts Awards for the 17th year running. We also celebrated winning Best Sustainable Fund Launch at the Sustainable Investment Awards 2025 for our Global Sustainable Government Bond Fund. In addition, we were Highly Commended for Investment Group of the Year for Diversity and Inclusion at the Women in Investment Awards 2025.

EdenTree is based in the heart of the City of London, but our team serves the professional investor community across the entirety of the UK, with dedicated regional sales managers providing exceptional levels of client support.

EdenTree is part of the Benefact Group – a charity owned, international family of specialist financial services companies that give all available profits to charity and good causes.

For investment professionals only. The value of an investment and the income from it may go down as well as up and the investor may not get back the amount invested.

For investment professionals only. This financial promotion issued by EdenTree Investment Management Limited (EdenTree) Reg No. 2519319. Registered in England at Benefact House, 2000, Pioneer Avenue, Gloucester Business Park, Brockworth, Gloucester, GL3 4AW, United Kingdom. EdenTree is authorised and regulated by the Financial Conduct Authority and is a member of the Investment Association. Firm Reference Number 527473. MKT001230